Key Takeaways

- You do not have to pay federal income tax on rental earnings if you rent your home for 14 days or fewer per year and use it personally for more than 14 days (or 10% of the rental period).

- You will only receive a Form 1099-K if you exceed $20,000 in gross payments and 200 transactions. For direct payments, the 1099-NEC threshold has increased to $2,000.

- You can deduct 100% of the cost of new furniture, appliances, and certain interior improvements in the very first year, rather than spreading the deduction over several years.

- If your average guest stay is 7 days or fewer and you “materially participate” in the management, you may be able to use your rental losses (like depreciation) to directly offset your W-2 salary income.

- While you pay income tax on profits, you are also responsible for collecting local occupancy taxes from guests.

The 2026 FIFA World Cup kicks off (see what I did there) in just a few weeks.

And if you’ve decided to list your Surprise, AZ home or spare room on Airbnb or VRBO to capitalize on the influx of global fans, I want to make sure you’re prepared for the tax side of short-term rental income.

Or, even if you’re just renting out a beach house or lakeside cabin for the season, understanding the tax rules around short-term rentals is the difference between keeping your hard-earned profits and handing an unnecessary chunk over to the IRS.

Do you have to pay short-term rental income taxes?

In the eyes of the IRS and state taxing authorities, once you begin charging guests to stay in your house, apartment, or even just a spare bedroom, you are officially a landlord. This means the money you earn is considered taxable income.

However, the taxability of your rental depends heavily on how many days the property is occupied by guests versus how many days you use it yourself.

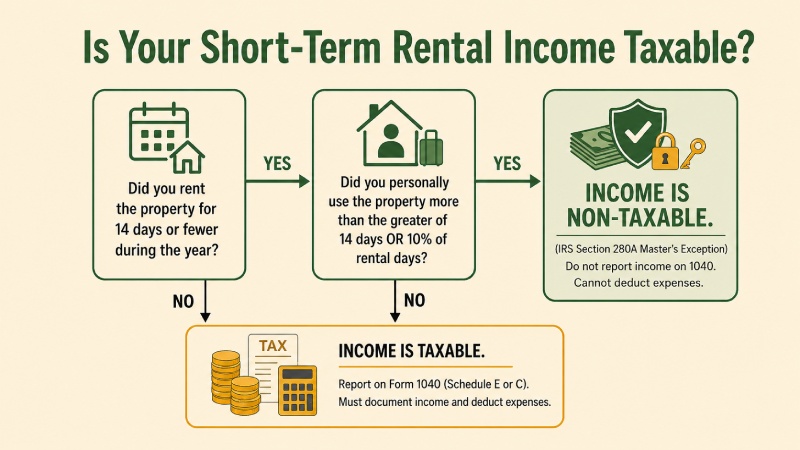

What’s the 14-day rule for short-term rental income taxes?

Commonly known as the “Master’s Exception,” the 14-day rule is the primary way you can avoid paying federal income tax on your rental earnings. But you must meet both of the following criteria:

- You rent the property out for no more than 14 days total during the tax year.

- You use the property yourself for more than the greater of:

- 14 days, or

- 10% of the total days it is rented at a fair market value

If you meet these two conditions, the IRS essentially treats the rental as non-existent for tax purposes. You don’t report the income, but you also can’t deduct any rental-related expenses.

If you rent your space for 15 days or more, you have officially entered the realm of landlord status. At this point:

- Every dollar earned must be reported on your federal and state tax returns.

- This income is subject to standard income tax rates.

- You become eligible to deduct the ordinary and necessary expenses of managing the rental.

What are occupancy taxes?

Beyond federal and state income taxes, you must also be aware of occupancy taxes. Sometimes referred to as tourist tax, hotel tax, or room or lodging tax.

Unlike income tax (which you pay on your profits), an occupancy tax is a percentage of the rental price paid by the guest and collected by you or the platform.

The rates and registration requirements vary wildly by city and county. Before you list your space, check your local ordinances to ensure you are collecting and remitting the correct amount to your local government. Failure to do so can lead to hefty penalties, regardless of how much you earned.

How to report short-term rental income

If you don’t meet the requirements of the IRS 14-day rule, you must report your rental earnings on your tax return. So, the first thing I look at as a tax pro is how you’re hosting. Because that determines which tax form we use.

There are two primary classifications for reporting this income:

- Schedule E (Supplemental Income and Loss): This is the most common classification for rental owners. You’ll report here if your rental is a passive activity. Meaning, you provide basic utilities and maintenance, but not “substantial services” during a guest’s stay.

- Schedule C (Profit or Loss from Business): Your rental shifts into this category if you provide substantial services beyond basic upkeep, like daily linen changes, guest meals, or concierge tours. This triggers an extra 15.3% tax hit on your profits and forces you onto Schedule C. (If you’re aiming for maximum margin, it’s usually better to stick to basic maintenance and avoid these substantial services.)

Because of federal reporting laws, rental platforms are required to share your earnings data with the IRS. Depending on your volume, you may receive one of two forms:

- Form 1099-K. This reports the gross payments you received through the platform. Under current 2026 rules, platforms only issue this form if you earn over $20,000 and have more than 200 transactions.

- Form 1099-NEC. This form is for non-employee compensation. The 2026 threshold for 1099-NEC reporting has increased to $2,000. (And don’t forget: this rule applies to you, too. If you pay a cleaner or contractor more than $2,000 directly this year, you’re responsible for issuing that 1099.)

Sometimes, a platform might send a 1099 to the IRS even if you rented your place for fewer than 14 days (especially if you live in a state with lower reporting thresholds).

This is why I tell every client to treat their rental like a business from day one. Keep a meticulous log of:

- Every date the property was rented.

- Every date you used the property personally.

- Detailed receipts for all related expenses.

Clear records make it easy to prove you meet the 14-day “Master’s Exception” or to accurately divide expenses between personal and business use for longer rentals.

What short-term rental tax deductions can you take?

The tax code allows you to deduct ordinary and necessary expenses to lower your taxable profit. Essentially, you only pay taxes on your net income (what’s left after expenses), not the total amount guests paid.

Here are the most common deductions I look for when reviewing a client’s rental portfolio:

- Cleaning and maintenance: This includes professional cleaning fees, laundry services, and any cleaning supplies (detergent, soaps, vacuums) you purchase yourself.

- Insurance: You can deduct premiums for property insurance and Private Mortgage Insurance (PMI).

- Utilities: Water, gas, electricity, internet, and TV/streaming services are all deductible for the periods the property is available for rent.

- Advertising: Any costs associated with marketing your listing, including professional photography.

- Repairs: Fixes like repairing a leaky faucet or replacing a broken window are fully deductible in the year they occur.

- Platform fees (like the guest or host-service fees charged by Airbnb or VRBO): Since your 1099 form typically reports the gross amount the guest paid, you must manually deduct these service fees on your return. Because 100% of these fees are directly related to the business of renting, you should deduct the entire amount.

Depreciation also allows you to write off the cost of the property (excluding land) and its furnishings over time.

And because of the OBBBA, 100% bonus depreciation allows you to potentially deduct the entire cost of furniture, appliances, and certain interior improvements in the very first year they are placed in service, rather than spreading the cost over several years.

How do you deduct mixed-use properties?

If you are renting out a spare room or a home you also live in, you can’t deduct the entire house’s expenses. Instead, you must allocate them:

- By space: If you rent one bedroom in a four-bedroom house, you generally deduct 25% of the shared expenses (like the roof repair or whole-house utilities).

- By time: If you rent the whole house for 60 days a year and live in it for the rest, you can only deduct expenses for that 60-day window.

What is the short-term rental taxes loophole?

Essentially, this strategy allows high-earning W-2 employees or business owners to use losses from their rental property to directly offset their other income, potentially saving a lot in taxes.

Normally, the IRS (under Section 469) classifies all rental income as passive. This is a problem because passive losses can only offset passive income. If your rental shows a loss due to depreciation but you have a $200,000 salary, that loss usually just sits there, suspended for future years. You can’t use it to lower the taxes on your paycheck.

The “loophole” exists because the IRS does not consider a property a rental activity if the average guest stay is 7 days or fewer. In this case, the property is treated as a business. If you materially participate in that business, your losses become non-passive.

Non-passive losses can offset your W-2 wages dollar-for-dollar.

Do I qualify for the short-term rental loophole?

To qualify, you must pass both of these tests:

- The average stay for all your guests during the year must be 7 days or fewer.

- Material Participation: You must prove your material participation. While there are seven tests, these are the three most common paths:

- You spent more than 500 hours on the short-term rental during the year.

- You did almost all the work yourself (no property manager, no regular cleaning crew).

- You spent at least 100 hours on the activity and more time than any other individual (including your cleaners or contractors).

- You spent more than 500 hours on the short-term rental during the year.

Imagine you earn a $150,000 salary. You buy a short-term rental, perform a cost segregation study, and meet the material participation requirements.

Gross W-2 Income: $150,000

STR Depreciation Loss: -$127,000

New Taxable Income: approximately $23,000

By using the loophole, you’ve effectively shielded nearly your entire salary from federal income tax for the year.

However, here’s my obligatory tax pro warning: If you claim this, you must keep a contemporaneous time log. If your log looks like it was written in one sitting with rounded-off numbers, an auditor will treat it as a ballpark estimate and likely disqualify your hours. To protect your W-2 offset, you need a record that was built week-by-week, backed up by receipts and digital timestamps.

Final thoughts

We’re approaching summer. Which means you’re entering the highest-volume period for logging the material participation hours needed to legally offset your W-2 income.

On top of that, the June 15th Q2 estimated tax deadline is coming up. Your summer bookings may push your income higher than you projected, which could lead to an ugly underpayment penalty next spring.

I’m currently opening spots for mid-year strategy sessions to audit your participation logs and calculate your Q2 payments so there are no surprises in April. Let’s get your session on the calendar:

app.acuityscheduling.com/schedule.php?owner=16680567

FAQs

“Airbnb says they have collected and remitted some taxes on our behalf, but we can’t find where or to whom those taxes were actually paid?”

Platforms like Airbnb and VRBO often collect state-level sales or occupancy taxes, but they may not collect local city or county-level taxes. To find exactly what was paid, look at your “Gross Earnings” report or your Transaction History on the platform. You’ll see line items for “Occupancy Tax” or “Pass-through Tax.” These are usually paid to the state’s Department of Revenue. If you don’t see a specific local tax listed there, you are likely responsible for filing and paying that yourself to your local municipality.

“Do you have to pay taxes on Airbnb rentals?”

If you rent your Maricopa County property for more than 14 days in a calendar year, the income is taxable at both the federal and state levels. If you stay under that 14-day limit (the “Master’s Exception”), you typically don’t pay federal income tax on that money, but remember that occupancy taxes (local tourist taxes) still apply from day one.

“Do I need to report my Airbnb income under $20,000?”

For 2026, the OBBBA has restored the 1099-K reporting threshold to $20,000 and 200 transactions. This means if you earned $15,000, you likely won’t receive a tax form from Airbnb, but you are still legally required to report that income. The IRS considers all income taxable, regardless of whether a platform sends you a piece of paper.

“Does hosting on Airbnb or VRBO make you self-employed?”

It depends on the services you provide. If you just provide a space, utilities, and basic cleaning between guests, you are a landlord and report on Schedule E (no self-employment tax). However, if you provide “substantial services” like daily cleaning while guests are there, breakfast, or guided tours, the IRS views you as a business owner. In that case, you report on Schedule C and will owe 15.3% self-employment tax.

“What are the tax deduction categories for short-term rental income?”

Keep receipts for:

- Operating Costs: Cleaning, laundry, and guest supplies.

- Utilities: Internet, TV, water, and electricity (prorated if you live there).

- Professional Fees: Service fees from Airbnb/VRBO, photography, and tax prep.

- Property Costs: Mortgage interest, property taxes, and insurance.

- Maintenance: Repairs, landscaping, and pest control.

“Should hosts do their own bookkeeping on QuickBooks or hire someone?”

If you have one property and it’s your first year, a well-organized spreadsheet or QuickBooks Self-Employed is often enough. However, once you have multiple properties or start trying to use the STR Loophole to offset your W-2 income, the complexity skyrockets. At that point, hiring a bookkeeper or a tax pro to oversee your records is an investment that pays for itself by preventing missed deductions and avoiding IRS red flags.

“When can we start claiming depreciation? Does it have to be after we officially list the Airbnb?”

You can start claiming depreciation the moment the property is “placed in service.” This means the property is ready and available to be rented, even if you haven’t secured your first booking yet. If you spent all of May renovating and listed it on June 1, your depreciation clock starts June 1.

“Will VRBO remit local taxes for me?”

VRBO has agreements with many states to collect statewide taxes, but thousands of small cities and counties require separate registration. Check the “Taxes” section in your VRBO dashboard. It will explicitly tell you which taxes they are collecting and which ones remain your responsibility. If it’s not listed as collected, you must register with your local tax authority and remit those payments yourself.